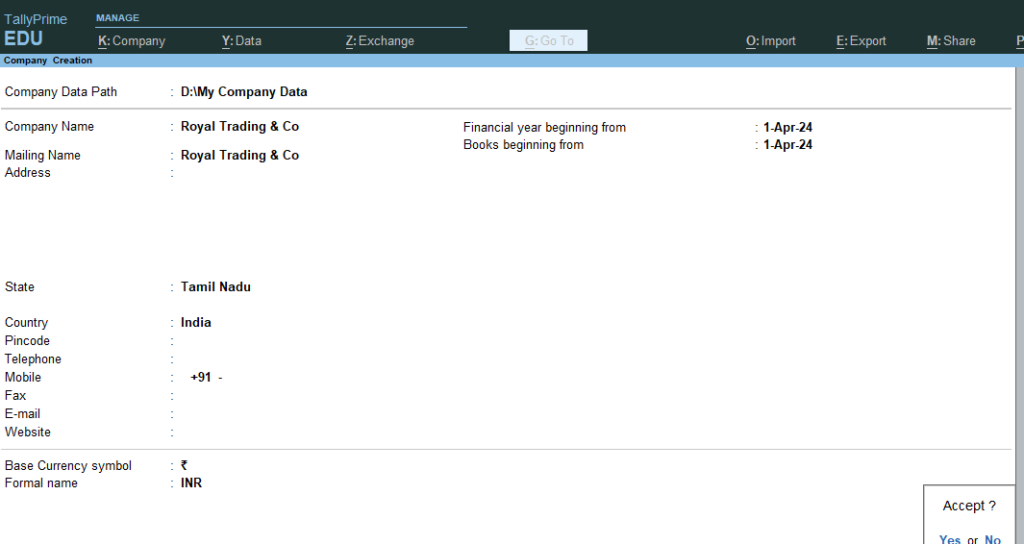

First Create a new company named Royal Trading & Co

2. After Company Creation > First Create the following ledgers >

Ledger Name

Group

Debit (₹)

Credit (₹)

Ramu Capital Account

Capital Account

10000

Cash in Hand

Cash-in-Hand

10000

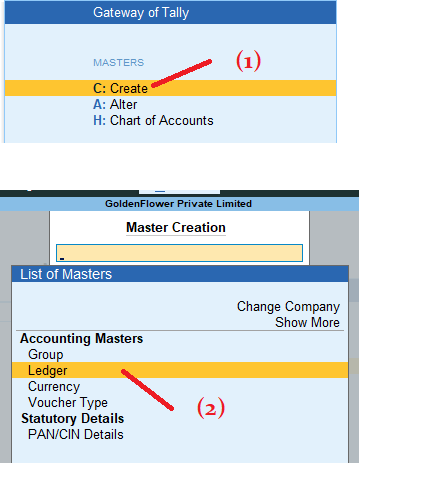

3. Gateway of Tally > Masters : Create > Ledgers:

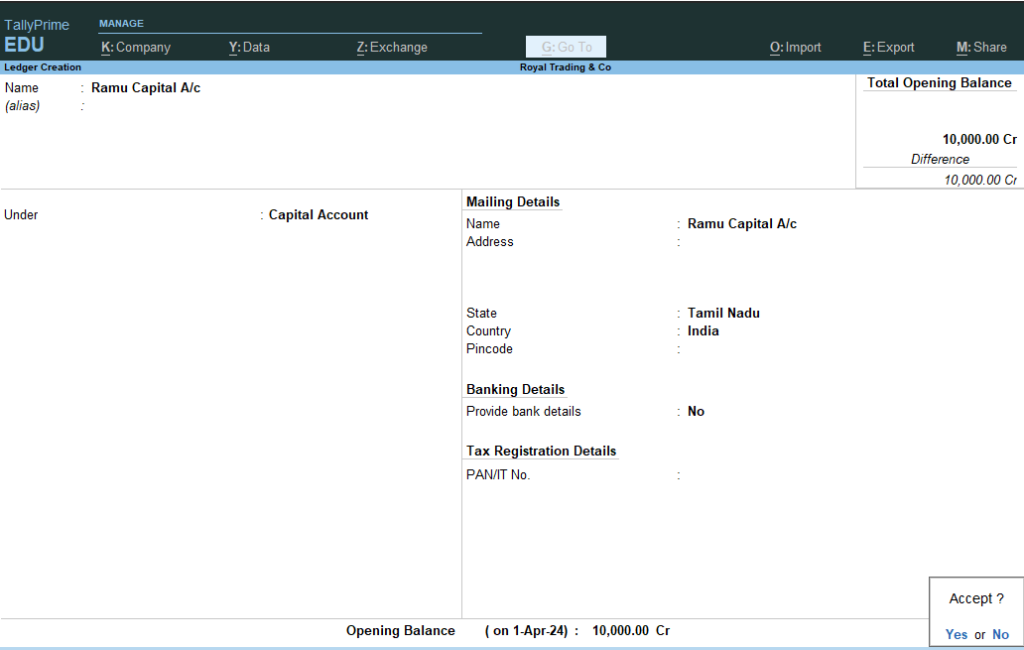

4. Enter Name : Ramu Capital A/c — Under : Type Cap and Select Right Side Using Arrow Keys or Select and Enter Capital Account > and Give Opening Balance : 10000 Cr. > Accept Yes >

5. Now you will see the Same Ledger creation > Press Escape twice and Goto Gateway of Tally >

6. Gateway of Tally > Master : Alter > Ledgers > Select Cash > Opening Balance : 10000 Dr.

7. So Ramu is Giver and Cash is Comes in to Business . So Cr. Ramu Capital A/c and Dr. Cash A/c

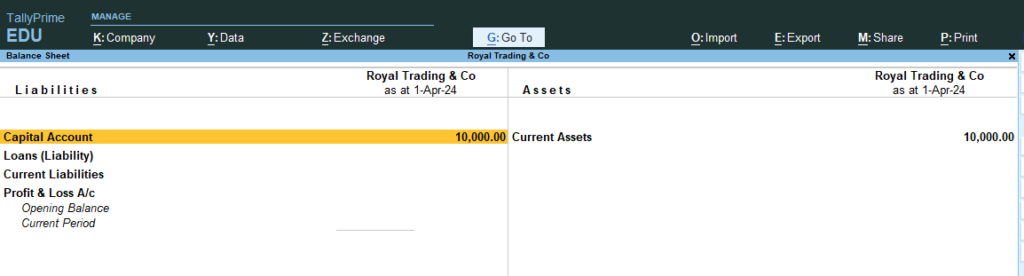

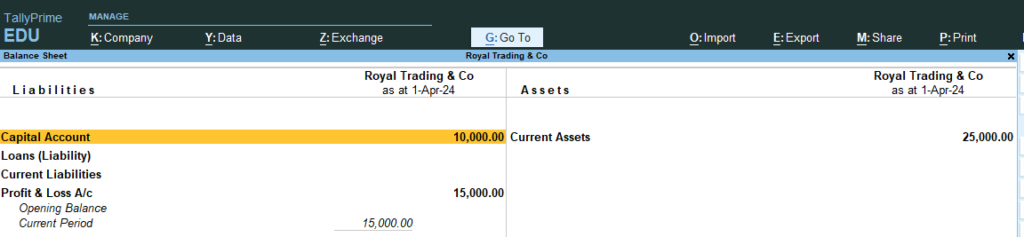

8. Go Gateway of Tally > Go Balance Sheet > You Can See Liabilities / Current Assets Statement

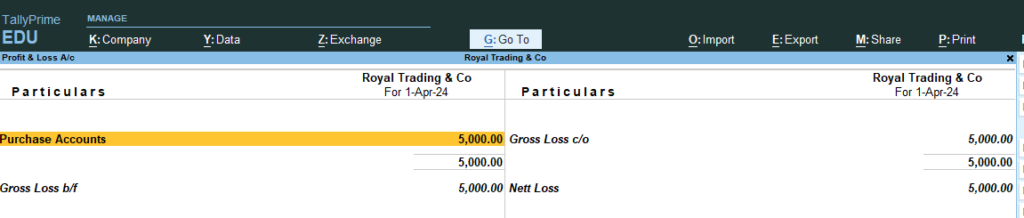

9. Go Gateway of Tally > Go Profit and Loss A/c > No Profit and Loss Data because no entry made in any purchase or sales

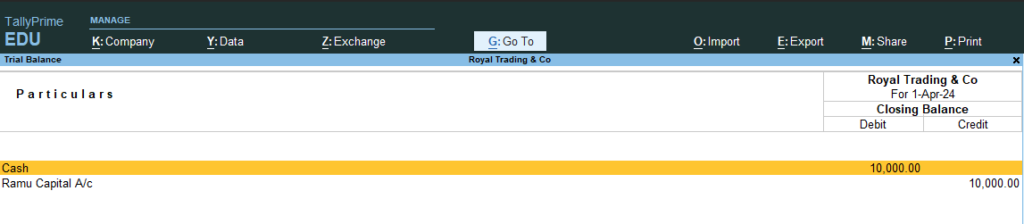

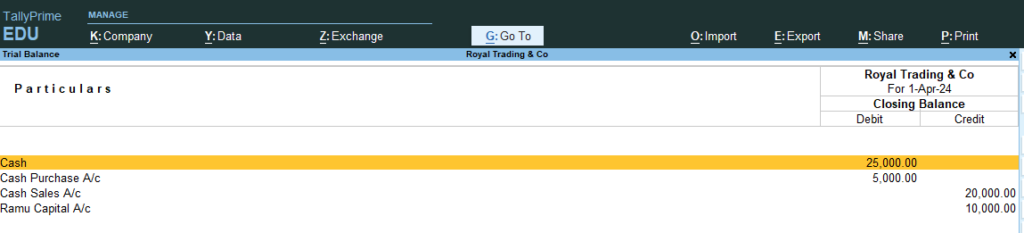

10. Go Gateway of Tally > Go Display More Reports or Press D > Go Trail Balance > and Press F5 (Ledger Wise / Group wise breakup)

11. Now Add the following Ledger

Ledger Name

Group

Debit (₹)

Credit (₹)

Cash Purchase A/c

Purchase

5000

Go Gateway of Tally > Enter Name : Cash Purchase A/c — Under : Select Purchase Account > and Give Opening Balance : 5000 Cr. > Accept Yes >

Gateway of Tally > Master : Alter > Ledgers > Select Cash > Opening Balance : 5000 Dr. (Because Amount to be reduced due to Cash purchase Rs.5000)

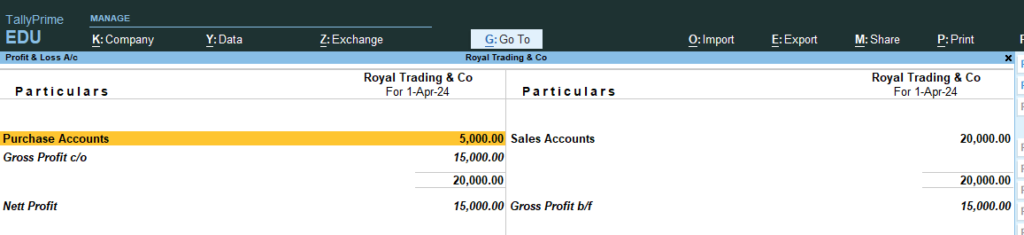

12. Now Go the Step No 8 , 9, 10 (See the changes in Profit and Loss and Balance sheet , now net loss Because Only Cash Purchase Not Sales ..)

13. Now Add the following Ledger

Ledger Name

Group

Debit (₹)

Credit (₹)

Cash Sales A/c

Sales

20000

Go Gateway of Tally > Master > Create : Ledgers > Enter Name : Cash Sales A/c — Under : Select Sales Account > and Give Opening Balance : 20000 Dr. > Accept Yes >

Gateway of Tally > Master : Alter > Ledgers > Select Cash > Opening Balance : 25000 Dr. (Because Amount to be raised due to Cash Sales Rs.20000)

14. Now Go the Step No 8 , 9, 10 (See the changes in Profit and Loss and Balance sheet)

Profit and Loss A/c

Balance Sheet

Trail Balance

13. Now Add the following Ledger

Ledger Name

Group

Debit (₹)

Credit (₹)

Furniture

Fixed Asset

5000

Telephone Charges

Indirect Expenses

1000

Electricity Bill Paid

Indirect Expenses

500

Total

6500

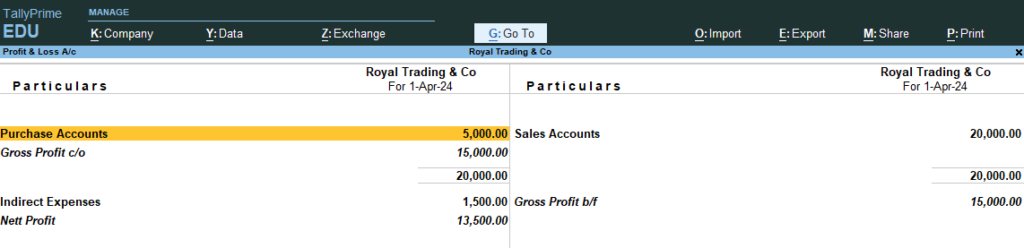

14. Go Gateway of Tally > Master > Create : Ledgers > Name : Furniture — Under : Fixed Asset > and Give Opening Balance : 5000 Dr. > Accept Yes >

15. Name : Telephone Charges — Under : Indirect Expenses > and Give Opening Balance : 1000 Dr.

16. Name : Electricity Bill Paid — Under : Indirect Expenses > and Give Opening Balance : 500 Dr.

17, Gateway of Tally > Master : Alter > Ledgers > Select Cash > Opening Balance : 18500 Dr. (Because Amount to be reduced due to Expenses (25000- 6500 = 18500 Dr.)

18. Now Go the Step No 8 , 9, 10 (See the changes in Profit and Loss and Balance sheet)

For a service-oriented organization using Tally Prime, the ledger and group setup will focus on managing revenue from services, handling expenses, and tracking other financial activities specific to service-based operations. Here’s a structured approach for setting up these ledgers and groups:

1. Groups

Group Name

Description

Sundry Debtors

Ledgers for clients or customers who owe payment for services rendered.

Sundry Creditors

Ledgers for suppliers or service providers.

Income

Revenues from various services provided.

Expenses

Various expenses including operational and administrative costs.

Fixed Assets

Assets such as office equipment and furniture.

Cash

Cash transactions and balances.

Bank

Transactions related to bank accounts.

2. Ledgers

Group

Ledger Name

Description

Sundry Debtors

Client A Receivables

Ledger for a specific client who owes payment.

Client B Receivables

Ledger for another client.

Sundry Creditors

Supplier A

Ledger for a specific supplier (e.g., office supplies).

Service Provider A

Ledger for service providers (e.g., IT support, consultancy).

Income

Service Income

Revenue from the services provided (e.g., consulting fees).

Project Income

Revenue from specific projects or contracts.

Other Income

Other sources of income (e.g., interest, miscellaneous revenue).

Expenses

Salaries and Wages

Salaries and wages for employees and contractors.

Rent

Expense for renting office space.

Utilities

Costs for utilities like electricity and water.

Office Supplies

Costs for office supplies and materials.

Travel Expenses

Costs related to travel for business purposes.

Professional Fees

Costs for professional services (e.g., legal, accounting).

Fixed Assets

Office Equipment

Ledger for office equipment (e.g., computers, printers).

Furniture

Ledger for office furniture.

Leasehold Improvements

Ledger for improvements made to leased premises.

Cash

Petty Cash

Small cash transactions and expenses.

Bank

Bank Account 1

Ledger for a specific bank account.

Bank Account 2

Ledger for another bank account.

This setup helps service-oriented organizations track their revenue from services, manage expenses related to operations, and maintain accurate records of financial transactions.

2) For retail or supermarkets

For retail or supermarkets using Tally Prime, organizing ledgers and groups in a table format can help manage various aspects of financial transactions and inventory. Here’s a structured view of how you might set up ledgers and groups for a retail or supermarket business:

1. Groups

Group Name

Description

Sundry Debtors

Ledgers for customers who owe money for purchased goods.

Sundry Creditors

Ledgers for suppliers/vendors to whom payments are owed.

Stock-in-Hand

Manages inventory or stock.

Sales

Revenue from sales transactions.

Purchases

Costs related to buying inventory.

Indirect Expenses

Expenses not directly tied to goods sold (e.g., rent, utilities).

Direct Expenses

Expenses directly related to the purchase of inventory (e.g., freight).

Fixed Assets

Assets used in the business such as machinery and furniture.

Cash

Cash transactions and balances.

Bank

Transactions related to bank accounts.

2. Ledgers

Group

Ledger Name

Description

Sundry Debtors

Customer A

Individual customer ledger.

Customer B

Another customer ledger.

Sundry Creditors

Supplier A

Ledger for a specific supplier.

Supplier B

Ledger for another supplier.

Stock-in-Hand

Groceries

Ledger for groceries stock.

Electronics

Ledger for electronic goods stock.

Sales

Cash Sales

Revenue from cash sales.

Credit Sales

Revenue from sales on credit.

Purchases

Inventory Purchase

Cost of purchasing inventory.

Freight Charges

Costs related to transporting goods.

Indirect Expenses

Rent

Expense for renting store premises.

Utilities

Expenses for utilities like electricity and water.

Office Supplies

Costs for office-related supplies.

Direct Expenses

Purchase Freight

Freight charges directly related to purchasing goods.

Packaging Costs

Costs for packaging materials.

Fixed Assets

Store Equipment

Ledger for equipment like cash registers, shelves, etc.

Furniture

Ledger for store furniture.

Cash

Petty Cash

Small cash transactions and expenses.

Bank

Bank Account 1

Ledger for a specific bank account.

Bank Account 2

Ledger for another bank account.

This setup will help you track sales, purchases, inventory, expenses, and bank transactions efficiently, making it easier to manage and report on the financial aspects of a retail or supermarket business.

3) For Manufacturing companies

For manufacturing companies using Tally Prime, the ledger and group setup will focus on tracking production costs, inventory, and other operational expenses. Here’s how you might organize these ledgers and groups in a table format:

1. Groups

Group Name

Description

Sundry Debtors

Ledgers for customers who owe money for goods sold.

Sundry Creditors

Ledgers for suppliers/vendors from whom materials are purchased.

Stock-in-Hand

Manages inventory of raw materials, work-in-progress, and finished goods.

Sales

Revenue from sales of finished products.

Purchases

Costs related to buying raw materials and other inputs.

Direct Expenses

Expenses directly related to production (e.g., direct labor, raw materials).

Indirect Expenses

Expenses not directly tied to production (e.g., rent, utilities).

Fixed Assets

Assets used in manufacturing such as machinery and equipment.

Cash

Cash transactions and balances.

Bank

Transactions related to bank accounts.

2. Ledgers

Group

Ledger Name

Description

Sundry Debtors

Customer A

Individual customer ledger.

Customer B

Another customer ledger.

Sundry Creditors

Supplier A

Ledger for a specific supplier.

Supplier B

Ledger for another supplier.

Stock-in-Hand

Raw Materials

Ledger for raw materials used in production.

Work-in-Progress

Ledger for partially completed products.

Finished Goods

Ledger for finished products ready for sale.

Sales

Domestic Sales

Revenue from sales within the country.

Export Sales

Revenue from sales to other countries.

Purchases

Raw Material Purchases

Cost of purchasing raw materials.

Packing Material Purchases

Cost of packing materials.

Direct Expenses

Direct Labor

Wages and salaries directly tied to production.

Production Supplies

Costs for supplies used directly in manufacturing.

Indirect Expenses

Rent

Expense for renting factory or office space.

Utilities

Costs for utilities such as electricity, water, etc.

Administrative Expenses

Costs related to administrative functions.

Fixed Assets

Machinery

Ledger for machinery used in production.

Equipment

Ledger for production equipment.

Cash

Petty Cash

Small cash transactions and expenses.

Bank

Bank Account 1

Ledger for a specific bank account.

Bank Account 2

Ledger for another bank account.

This setup helps track the various aspects of manufacturing operations, including inventory management, production costs, sales, and financial transactions, making it easier to manage and analyze financial data.

4) For schools and Collages

For schools using Tally Prime, the ledger and group setup will focus on managing finances related to tuition fees, salaries, utilities, and other school-related expenses. Here’s how you might organize these ledgers and groups in a table format:

1. Groups

Group Name

Description

Sundry Debtors

Ledgers for students or parents who owe tuition fees.

Sundry Creditors

Ledgers for vendors or suppliers providing services or materials.

Income

Revenue from sources like tuition fees and donations.

Expenses

Various expenses incurred by the school.

Fixed Assets

Assets such as buildings, furniture, and equipment.

Cash

Cash transactions and balances.

Bank

Transactions related to bank accounts.

2. Ledgers

Group

Ledger Name

Description

Sundry Debtors

Student Fees Receivable

Ledger for tracking tuition fees owed by students.

Parent Fees Receivable

Ledger for fees receivable from parents.

Sundry Creditors

Supplier A

Ledger for a specific supplier (e.g., stationery supplier).

Service Provider A

Ledger for service providers (e.g., cleaning services).

Income

Tuition Fees

Revenue from student tuition fees.

Donations

Income from donations and grants.

Miscellaneous Income

Other sources of income (e.g., event fees).

Expenses

Salaries and Wages

Salaries and wages for teachers and staff.

Utilities

Expenses for electricity, water, and other utilities.

Stationery and Supplies

Costs for educational supplies and stationery.

Maintenance Costs

Expenses for maintaining school facilities.

Fixed Assets

Building

Ledger for school buildings and property.

Furniture and Fixtures

Ledger for classroom and office furniture.

Educational Equipment

Ledger for equipment like computers, projectors, etc.

Cash

Petty Cash

Small cash transactions and expenses.

Bank

Bank Account 1

Ledger for a specific bank account.

Bank Account 2

Ledger for another bank account.

This setup helps schools manage their financial transactions efficiently, including tracking income from tuition fees, managing expenses related to operations, and handling bank and cash transactions.

5) For government organizations

For government organizations using Tally Prime, the ledger and group setup will focus on managing public funds, tracking expenditures, handling revenues, and maintaining transparency. Here’s a structured approach for setting up these ledgers and groups:

1. Groups

Group Name

Description

Sundry Debtors

Ledgers for receivables from other government entities or departments.

Sundry Creditors

Ledgers for payments owed to suppliers and contractors.

Income

Revenues from various sources such as grants, taxes, and fees.

Expenditure

Various expenditures including operational and project costs.

Fixed Assets

Assets like buildings, equipment, and infrastructure.

Cash

Cash transactions and balances.

Bank

Transactions related to bank accounts.

2. Ledgers

Group

Ledger Name

Description

Sundry Debtors

Receivables from Department A

Amounts receivable from other government departments.

Receivables from External Agencies

Amounts receivable from external entities or agencies.

Sundry Creditors

Supplier A

Ledger for a specific supplier or contractor.

Service Provider A

Ledger for service providers (e.g., maintenance services).

Income

Grants and Subsidies

Revenue from grants and subsidies provided by higher authorities.

Tax Revenues

Revenues from various taxes (e.g., property tax, sales tax).

Fees and Charges

Income from fees for services provided (e.g., registration fees).

Costs related to specific government projects or initiatives.

Maintenance Costs

Expenses for maintaining government properties and equipment.

Fixed Assets

Buildings

Ledger for government buildings and infrastructure.

Office Equipment

Ledger for office equipment and furniture.

Vehicles

Ledger for government vehicles.

Cash

Petty Cash

Small cash transactions and expenditures.

Bank

Bank Account 1

Ledger for a specific bank account.

Bank Account 2

Ledger for another bank account.

This setup ensures that government organizations can effectively manage their finances, track revenue and expenditures, and maintain transparency and accountability in their financial reporting.

6) For municipalities, corporations, or town panchayats

For municipalities, corporations, or town panchayats using Tally Prime, the ledger and group setup will help manage public funds, track expenditures, and handle various local government functions. Here’s how you might organize these ledgers and groups:

1. Groups

Group Name

Description

Sundry Debtors

Ledgers for amounts receivable from residents and businesses (e.g., property tax arrears).

Sundry Creditors

Ledgers for payments owed to suppliers, contractors, and service providers.

Income

Revenues from various sources such as taxes, fees, and grants.

Expenditure

Various expenditures including operational costs and project expenses.

Fixed Assets

Assets like buildings, equipment, and infrastructure.

Cash

Cash transactions and balances.

Bank

Transactions related to bank accounts.

2. Ledgers

Group

Ledger Name

Description

Sundry Debtors

Property Tax Receivables

Amounts receivable from property owners for taxes.

Water Charges Receivable

Amounts receivable from residents for water charges.

Municipal Fees Receivable

Amounts receivable from various municipal services.

Sundry Creditors

Supplier A

Ledger for a specific supplier (e.g., for materials or services).

Contractor A

Ledger for contractors providing construction or maintenance services.

Service Provider A

Ledger for service providers (e.g., waste management, street cleaning).

Income

Property Tax Income

Revenue from property taxes.

Water Revenue

Revenue from water charges.

Service Fees

Income from various municipal services (e.g., permits, licenses).

Grants and Subsidies

Income from grants and subsidies received from higher authorities.

Costs for maintaining public infrastructure and facilities.

Project Expenses

Expenses for specific municipal projects (e.g., road construction).

Fixed Assets

Buildings

Ledger for municipal buildings and facilities.

Street Lighting

Ledger for street lighting infrastructure.

Public Equipment

Ledger for equipment used for public services (e.g., vehicles).

Cash

Petty Cash

Small cash transactions and expenditures.

Bank

Bank Account 1

Ledger for a specific bank account.

Bank Account 2

Ledger for another bank account.

This setup will help municipalities, corporations, or town panchayats manage their financial activities efficiently, track income and expenditures, and maintain effective control over public funds and assets.

7) For trading companies

For trading companies using Tally Prime, the ledger and group setup will focus on managing inventory, sales, purchases, and related financial transactions. Here’s how you might organize these ledgers and groups:

1. Groups

Group Name

Description

Sundry Debtors

Ledgers for customers who owe money for goods sold.

Sundry Creditors

Ledgers for suppliers from whom inventory is purchased.

Stock-in-Hand

Manages inventory of goods for resale.

Sales

Revenue from sales transactions.

Purchases

Costs related to buying inventory.

Direct Expenses

Expenses directly tied to the procurement and sale of goods.

Indirect Expenses

Expenses not directly tied to the sale of goods (e.g., rent, utilities).

Fixed Assets

Assets such as buildings, furniture, and equipment.

Cash

Cash transactions and balances.

Bank

Transactions related to bank accounts.

2. Ledgers

Group

Ledger Name

Description

Sundry Debtors

Customer A

Ledger for a specific customer.

Customer B

Ledger for another customer.

Sundry Creditors

Supplier A

Ledger for a specific supplier.

Supplier B

Ledger for another supplier.

Stock-in-Hand

Inventory – Goods

Ledger for tracking goods available for sale.

Raw Materials

Ledger for raw materials if involved in manufacturing.

Sales

Domestic Sales

Revenue from sales within the country.

Export Sales

Revenue from sales to other countries.

Purchases

Inventory Purchases

Cost of purchasing goods for resale.

Freight Charges

Cost of transporting goods.

Direct Expenses

Purchase Expenses

Costs directly related to purchasing inventory (e.g., freight, handling).

Packaging Costs

Costs for packaging materials.

Indirect Expenses

Rent

Expense for renting office or warehouse space.

Utilities

Costs for utilities such as electricity and water.

Office Supplies

Costs for office-related supplies.

Advertising

Costs for advertising and marketing.

Fixed Assets

Building

Ledger for buildings and real estate.

Furniture and Fixtures

Ledger for office furniture and fixtures.

Equipment

Ledger for machinery and other equipment.

Cash

Petty Cash

Small cash transactions and expenditures.

Bank

Bank Account 1

Ledger for a specific bank account.

Bank Account 2

Ledger for another bank account.

This setup will help trading companies manage their financial transactions effectively, keep track of inventory and sales, and handle both direct and indirect expenses.

Organizations can be classified into various types based on their structure, ownership, and objectives. Here’s an overview of different types of organizations:

Sole Proprietorship Description: Owned and operated by a single individual. Characteristics: Simple to set up, owner has complete control, unlimited liability. Examples: Local small businesses, freelance professionals.

Partnership Description: Owned by two or more individuals who share profits and responsibilities. Characteristics: Shared management, limited liability (in limited partnerships), profits and losses shared as per the partnership agreement. Examples: Law firms, accounting firms, medical practices.

Limited Liability Partnership (LLP) Description: A partnership where some or all partners have limited liabilities. Characteristics: Combines elements of partnerships and corporations, protects individual partners from personal liability. Examples: Professional services firms, startups.

Private Limited Company (Ltd) Description: A privately held company with limited liability. Characteristics: Owned by a small group of investors, shares are not publicly traded, limited liability for shareholders. Examples: Small to medium-sized enterprises, family businesses.

Public Limited Company (PLC) Description: A company whose shares are traded on a stock exchange and are available to the public. Characteristics: Limited liability, can raise capital by issuing shares, regulated by stock exchange laws. Examples: Large corporations like Apple, Microsoft.

Non-Profit Organization (NPO) Description: An organization that operates for charitable, educational, or other socially beneficial purposes rather than for profit. Characteristics: Exempt from income taxes, must reinvest surplus funds into the organization’s mission. Examples: Charities, foundations, educational institutions.

Cooperative Description: An organization owned and operated by its members, who share the profits or benefits. Characteristics: Members have equal voting rights, profits are distributed among members. Examples: Agricultural cooperatives, credit unions, housing cooperatives.

Government Organization Description: Entities created and operated by the government to provide public services. Characteristics: Funded by taxpayer money, not-for-profit, serves public interests. Examples: Public schools, municipal services, government agencies.

State-Owned Enterprise (SOE) Description: A business owned and operated by the government. Characteristics: May operate like a private corporation but is controlled by government policies. Examples: National airlines, utilities companies.

Joint Venture Description: A business arrangement where two or more parties agree to pool their resources for a specific project or purpose. Characteristics: Shared risk and reward, separate legal entity, typically for a limited time. Examples: Collaborative projects between companies, international business collaborations.

Franchise Description: A business model where an individual or group is granted the right to operate a business using the branding and business model of an established company. Characteristics: Franchisee operates independently but under the franchisor’s brand and guidelines. Examples: Fast-food chains like McDonald’s, retail stores like 7-Eleven.

Social Enterprise Description: An organization that applies commercial strategies to maximize improvements in human and environmental well-being. Characteristics: Focuses on social impact rather than profit, often reinvests profits to achieve social goals. Examples: Fair trade companies, businesses addressing social issues.

Mutual Benefit Association Description: An organization formed to provide benefits to its members, such as insurance or financial support. Characteristics: Members contribute to a common fund and receive benefits based on their contributions. Examples: Insurance companies, professional associations. Summary These types of organizations vary widely in their structure, purpose, and operational characteristics, and understanding these differences can help in recognizing their unique roles in the economy and society.

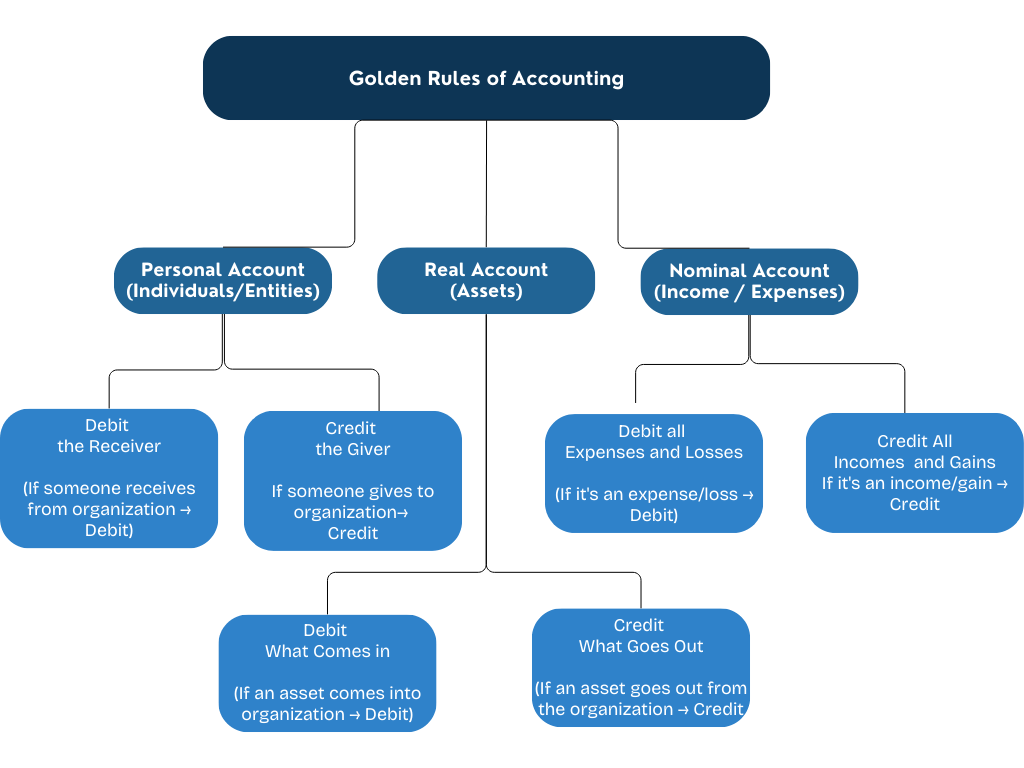

Ledger is like a detailed record or account that tracks all transactions related to a specific item or entity.

Think of it as a notebook where you write down everything that happens related to one thing, like all the money you spend on rent or all the sales you make.

Examples:

Cash Ledger: Tracks all cash transactions (money coming in and going out).

Sales Ledger: Tracks all the sales made by the business.

Salary Ledger: Tracks the payments made to employees.

What is a Group?

Group is a category that helps organize ledgers in Tally Prime.

It’s like a folder where similar types of ledgers are kept together. This makes it easier to manage and find them.

Groups help Tally Prime understand what kind of transactions are recorded in each ledger.

Examples:

Capital Account: This is a group of ledgers involving owners’ investment in the business.

Sundry Debtors: These are the various individuals or firms from whom the business has to recover.

Fixed Assets: A group containing ledgers for items owned by the business, like furniture or any type of machinery.

Why Use Ledgers and Groups?

Organized Record-Keeping: By using ledgers and groups, you can keep your financial records organized and easy to understand.

Accurate Reporting: Tally Prime can generate accurate financial reports, like balance sheets and profit & loss statements, based on the information in ledgers.

Simplifies Management: Groups help you manage similar accounts together, making it easier to analyze the financial health of the business.

Ledgers as a Diary:

This is how one can understand what a ledger is. A ledger is just like a diary where one writes everything concerning a particular subject. For example, you have a daily journal where you write down all your daily expenses. For example, you have a daily journal in which you write down all your expenses each day. Every page may be allocated to various spends one makes, such as food, travel, or entertainment.

Groups as Categories:

Now, these pages in your diary will be divided based on sections or categories. For example, you can have “Food,” another “Travel,” and another “Entertainment.” Then within each category, there are those sheets of pages where you write down the specifics. In accounting, these categories are termed “Groups”, with the sheets being “Ledgers.”

Example:

For example, one group could be “Expenses,” while sub-ledgers might include “Rent,” “Groceries,” or “Utilities.” All the transactions related to each particular expense would then be noted in its corresponding ledger.

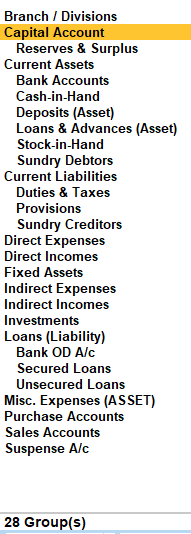

In Tally Prime, there are a total of 28 predefined groups. These groups are used to classify and organize ledgers according to their nature and purpose. Here’s a breakdown:

15 Primary Groups

These are the main groups under which all other groups and ledgers are classified.

Capital Account

Reserves & Surplus

Loans (Liability)

Current Liabilities

Current Assets

Fixed Assets

Investments

Branch/Divisions

Miscellaneous Expenses (Asset)

Suspense Account

Sales Accounts

Purchase Accounts

Direct Incomes

Direct Expenses

Indirect Incomes

13 Subgroups

These subgroups are categorized under the primary groups:

Sundry Creditors (Under Current Liabilities)

Sundry Debtors (Under Current Assets)

Cash-in-Hand (Under Current Assets)

Bank Accounts (Under Current Assets)

Loans & Advances (Asset) (Under Current Assets)

Duties & Taxes (Under Current Liabilities)

Provisions (Under Current Liabilities)

Stock-in-Hand (Under Current Assets)

Deposits (Asset) (Under Current Assets)

Secured Loans (Under Loans (Liability))

Unsecured Loans (Under Loans (Liability))

Branch/Division (Under Capital Account)

Suspense Account (Under Current Liabilities)

Custom Groups

You can also create custom groups based on specific business needs. These custom groups can be placed under any of the primary groups listed above.

Activity :

After Company Creation > Gateway to Tally > Under Masters > H: Chart of Accounts >Groups :

Here’s a detailed explanation of all 28 groups in Tally Prime, along with examples of ledgers that fall under each group:

1. Capital Account

Purpose: Tracks the owner’s equity or investment in the business and any withdrawals.

Examples:

Capital Ledger: Represents the owner’s investment.

Drawings Ledger: Tracks money withdrawn by the owner for personal use.

Amutha Capital a/c

Owner Name Capital A/c

2. Reserves & Surplus

Purpose: Represents accumulated profits retained in the business or any reserves.

Examples:

General Reserve Ledger: A reserve fund for future contingencies.

Profit & Loss Account: If there’s a profit carried forward from previous years.

3. Loans (Liability)

Purpose: Tracks borrowed funds that the business needs to repay.

Examples:

Bank Loan Ledger: Records loans taken from banks.

Debenture Ledger: Tracks money raised through debentures.

4. Current Liabilities

Purpose: Represents short-term obligations or debts that the business must pay within a year.

Examples:

Sundry Creditors Ledger: Money owed to suppliers or vendors.

Outstanding Expenses Ledger: Expenses that have been incurred but not yet paid.

5. Current Assets

Purpose: Represents assets that can be converted into cash within a year.

Examples:

Sundry Debtors Ledger: Tracks amounts receivable from customers.

Cash Ledger: Records all cash transactions.

6. Fixed Assets

Purpose: Represents long-term assets that the business owns, like property, machinery, etc.

Examples:

Building Ledger: Tracks the value of buildings owned.

Machinery Ledger: Represents the value of machinery used in the business.

7. Investments

Purpose: Tracks investments made by the business in other companies, stocks, bonds, etc.

Examples:

Shares Ledger: Records the purchase of shares in other companies.

Government Bonds Ledger: Tracks investments in government bonds.

8. Branch/Divisions

Purpose: Used to track accounts for different branches or divisions within the same company.

Examples:

Branch A Ledger: Records transactions specific to Branch A.

Division 1 Ledger: Tracks transactions related to a specific division within the company.

9. Miscellaneous Expenses (Asset)

Purpose: Represents expenses that are deferred and written off over a period of time.

Examples:

Preliminary Expenses Ledger: Records expenses incurred during the formation of the company.

Deferred Revenue Expenditure Ledger: Expenses to be written off gradually.

10. Suspense Account

Purpose: Used temporarily for transactions where the correct ledger is not yet determined.

Examples:

Suspense Ledger: Any uncertain or incomplete transactions are recorded here temporarily.

11. Sales Accounts

Purpose: Tracks income earned from selling goods or services.

Examples:

Domestic Sales Ledger: Records sales made within the country.

Export Sales Ledger: Tracks sales made to customers outside the country.

Sales A/c

Cash Sales A/c

Credit Sales A/c

12. Purchase Accounts

Purpose: Tracks the cost of goods or services purchased by the business.

Examples:

Local Purchases Ledger: Records purchases made from local suppliers.

Import Purchases Ledger: Tracks purchases made from foreign suppliers.

Purchase A/c

Cash Purchase A/c

Cash Sales A/c

Purchase Return A/c

13. Direct Incomes

Purpose: Represents income directly related to the core business activities.

Examples:

Commission Received Ledger: Tracks commission earned from sales.

Service Income Ledger: Records income from services provided.

Professional Charges A/c

Consulting Fees A/c

Service Charges A/c

14. Direct Expenses

Purpose: Represents expenses directly related to the production or purchase of goods.

Examples:

Freight Inwards Ledger: Tracks transportation costs for bringing goods into the business.

Raw Material Ledger: Records the cost of raw materials used in production.

Carriage inwards A/c

Wages A/c

15. Indirect Incomes

Purpose: Represents income from activities not directly related to the primary business operations.

Examples:

Interest Received Ledger: Tracks interest earned on deposits or investments.

Rental Income Ledger: Records income from renting out property or equipment.

Rent Received A/c

Interest Received A/c

Commission Received A/c

16. Indirect Expenses

Purpose: Represents expenses not directly related to the production of goods but necessary for running the business.

Examples:

Rent Ledger: Tracks payments made for renting office space.

Salary Ledger: Records payments made to employees.

Telephone Charges A/c

Bank Charges A/c

Rent Charges A/c

Electricity Expenses

17. Sundry Creditors (Under Current Liabilities)

Purpose: Tracks amounts owed to suppliers or vendors.

Examples:

Raja Suppliers Ledger: Records money owed to Raja Suppliers.

Kumar Traders Ledger: Tracks amounts payable to Kumar Traders.

Balram A/c

Rajan A/c

18. Sundry Debtors (Under Current Assets)

Purpose: Tracks money receivable from customers who purchased goods or services on credit.

Examples:

Suresh & Co Customer Ledger: Records amounts receivable from Customer Suresh & Co

Ramu A/c Ledger: Tracks money owed by Ramu A/c

19. Cash-in-Hand (Under Current Assets)

Purpose: Tracks all cash transactions of the business.

Examples:

Main Cash Ledger: Records cash held by the business.

Petty Cash Ledger: Tracks small cash expenses.

20. Bank Accounts (Under Current Assets)

Purpose: Tracks all transactions related to bank accounts.

Examples:

HDFC Bank Ledger: Records transactions with HDFC Bank.

ICICI Bank Ledger: Tracks transactions with ICICI Bank.

21. Loans & Advances (Asset) (Under Current Assets)

Purpose: Represents loans given by the business to others.

Examples:

Advance to Supplier Ledger: Records advance payments made to suppliers.

Loan to Employee Ledger: Tracks loans given to employees.

22. Duties & Taxes (Under Current Liabilities)

Purpose: Tracks amounts related to taxes and duties payable to the government.

Examples:

GST Ledger: Records Goods and Services Tax collected and payable.

Income Tax Ledger: Tracks the business’s income tax liability.

23. Provisions (Under Current Liabilities)

Purpose: Represents amounts set aside for future expenses or liabilities.

Examples:

Provision for Taxation Ledger: Tracks amounts set aside for tax payments.

Provision for Doubtful Debts Ledger: Records provisions made for bad debts.

24. Stock-in-Hand (Under Current Assets)

Purpose: Tracks the value of goods in stock.

Examples:

Finished Goods Ledger: Records the value of finished goods in inventory.

Raw Materials Ledger: Tracks the value of raw materials in stock.

25. Deposits (Asset) (Under Current Assets)

Purpose: Represents deposits made by the business that are expected to be returned.

Examples:

Security Deposit Ledger: Tracks deposits given for securing premises or equipment.

Fixed Deposit Ledger: Records fixed deposits made with banks.

26. Secured Loans (Under Loans (Liability))

Purpose: Tracks loans that are backed by collateral or security.

Examples:

Mortgage Loan Ledger: Records loans taken against property.

Car Loan Ledger: Tracks loans secured against a vehicle.

27. Unsecured Loans (Under Loans (Liability))

Purpose: Tracks loans that are not backed by any collateral.

Examples:

Personal Loan Ledger: Records personal loans taken by the business.

Overdraft Ledger: Tracks overdraft facilities provided by banks.

28. Branch/Division (Under Capital Account)

Purpose: Tracks accounts for different branches or divisions within the same company.

Examples:

Branch A Capital Ledger: Records the capital allocated to Branch A.

Division 1 Capital Ledger: Tracks the capital allocated to a specific division.

Group

Ledger Name

Purpose

Capital Account

Capital

Owner’s investment in the business.

Capital Account

Drawings

Owner’s withdrawals for personal use.

Capital Account

Partner A Capital

Capital contribution by Partner A.

Capital Account

Partner B Capital

Capital contribution by Partner B.

Reserves & Surplus

General Reserve

Accumulated profits set aside for future use.

Reserves & Surplus

Profit & Loss A/C

Profits or losses carried forward.

Reserves & Surplus

Retained Earnings

Profits retained in the business.

Reserves & Surplus

Dividend Reserve

Amount reserved for dividend distribution.

Loans (Liability)

Bank Loan

Loans taken from banks.

Loans (Liability)

Debentures

Funds raised through debentures.

Loans (Liability)

Loan from Directors

Loans taken from company directors.

Loans (Liability)

Mortgage Loan

Loans secured against property.

Current Liabilities

Sundry Creditors

Amounts payable to suppliers or vendors.

Current Liabilities

Outstanding Expenses

Expenses incurred but not yet paid.

Current Liabilities

Duties & Taxes

Taxes payable (e.g., GST, VAT).

Current Liabilities

Salary Payable

Salaries due but not yet paid.

Current Liabilities

TDS Payable

Tax Deducted at Source yet to be paid to the government.

Current Liabilities

GST Payable

Goods and Services Tax payable.

Current Liabilities

Professional Tax Payable

Professional tax due for payment.

Current Liabilities

Provident Fund Payable

Provident fund contributions due.

Current Assets

Sundry Debtors

Money receivable from customers.

Current Assets

Cash

Tracks all cash transactions.

Current Assets

HDFC Bank A/C

Transactions related to HDFC Bank.

Current Assets

ICICI Bank A/C

Transactions related to ICICI Bank.

Current Assets

Advance to Suppliers

Payments made in advance to suppliers.

Current Assets

Prepaid Insurance

Insurance premiums paid in advance.

Current Assets

Prepaid Rent

Rent paid in advance.

Current Assets

Petty Cash

Small cash expenses.

Current Assets

Advances to Employees

Money advanced to employees.

Current Assets

Bills Receivable

Bills that are due for payment from customers.

Current Assets

Fixed Deposit

Money deposited in fixed-term accounts.

Current Assets

Investments in Shares

Investments in company shares.

Fixed Assets

Building

Value of buildings owned by the business.

Fixed Assets

Machinery

Value of machinery used in the business.

Fixed Assets

Furniture & Fixtures

Value of office furniture and fixtures.

Fixed Assets

Computers

Value of computers and IT equipment.

Fixed Assets

Vehicles

Value of vehicles owned by the business.

Fixed Assets

Office Equipment

Value of office equipment (e.g., printers, fax machines).

Fixed Assets

Land

Value of land owned by the business.

Fixed Assets

Air Conditioning Equipment

Value of AC units installed in the office.

Fixed Assets

Tools & Equipment

Value of tools used in manufacturing or operations.

Investments

Shares in ABC Ltd.

Investment in shares of ABC Ltd.

Investments

Mutual Funds

Investments in mutual funds.

Investments

Government Bonds

Investments in government bonds.

Investments

Fixed Deposits

Fixed deposits with banks.

Investments

Real Estate Investment

Investments in real estate properties.

Investments

Investment in Subsidiary Company

Investment in a subsidiary company.

Investments

Investment in Partnership Firm

Investments in a partnership business.

Sales Accounts

Local Sales

Income from sales within the country.

Sales Accounts

Export Sales

Income from sales outside the country.

Sales Accounts

Sales of Services

Income from services provided.

Sales Accounts

Sales of Goods

Income from the sale of goods.

Sales Accounts

Sales Returns

Returns of sold goods.

Purchase Accounts

Local Purchases

Cost of goods purchased from local suppliers.

Purchase Accounts

Import Purchases

Cost of goods purchased from foreign suppliers.

Purchase Accounts

Purchase of Raw Materials

Cost of raw materials purchased for production.

Purchase Accounts

Purchase of Office Supplies

Cost of office supplies purchased.

Purchase Accounts

Purchase Returns

Returns of purchased goods.

Purchase Accounts

Freight Inwards

Cost of transportation for purchased goods.

Direct Incomes

Commission Received

Income from commissions earned on sales.

Direct Incomes

Service Income

Income from services provided.

Direct Incomes

Royalty Income

Income from royalties.

Direct Incomes

Interest on Loans Given

Interest earned on loans provided by the business.

Direct Incomes

Dividend Received

Dividends received from investments.

Direct Expenses

Freight Inwards

Transportation costs for bringing goods into the business.

Direct Expenses

Raw Material Purchases

Costs of raw materials used in production.

Direct Expenses

Power & Fuel

Expenses for power and fuel used in production.

Direct Expenses

Wages

Wages paid to labor directly involved in production.

Direct Expenses

Factory Rent

Rent for factory premises.

Indirect Incomes

Interest Received

Income from interest earned on deposits.

Indirect Incomes

Rental Income

Income from renting out property or equipment.

Indirect Incomes

Miscellaneous Income

Income from other sources not directly related to core business.

Indirect Incomes

Profit on Sale of Assets

Gain from the sale of fixed assets.

Indirect Incomes

Discount Received

Discounts received on purchases.

Indirect Expenses

Rent

Expenses related to renting office space.

Indirect Expenses

Salary

Payments made to employees.

Indirect Expenses

Office Expenses

General office expenses (e.g., stationery, utilities).

Indirect Expenses

Telephone Expenses

Costs of telephone and internet services.

Indirect Expenses

Travel Expenses

Expenses for business travel.

Indirect Expenses

Advertising Expenses

Costs related to marketing and advertising.

Indirect Expenses

Professional Fees

Payments made to professionals (e.g., lawyers, accountants).

Indirect Expenses

Insurance Premium

Costs of insurance for business assets.

Indirect Expenses

Repairs & Maintenance

Costs of maintaining and repairing business assets.

Indirect Expenses

Bad Debts

Amounts written off as unrecoverable debts.

Branch/Divisions

Branch A

Tracks transactions specific to Branch A.

Branch/Divisions

Branch B

Tracks transactions specific to Branch B.

Branch/Divisions

Division 1

Records transactions related to Division 1.

Branch/Divisions

Division 2

Records transactions related to Division 2.

Miscellaneous Expenses

Preliminary Expenses

Expenses incurred during the formation of the company.

Miscellaneous Expenses

Deferred Revenue Expenditure

Expenses to be written off gradually over time.

Miscellaneous Expenses

Promotional Expenses

Expenses for promoting new products or services.

Miscellaneous Expenses

Legal Fees

Legal costs that are amortized over time.

Secured Loans

Mortgage Loan

Loans secured against property.

Secured Loans

Car Loan

Loans secured against a vehicle.

Secured Loans

Equipment Loan

Loans secured against business equipment.

Secured Loans

Term Loan

Secured long-term loan.

Unsecured Loans

Personal Loan

Loans taken without any collateral.

Unsecured Loans

Overdraft

Bank overdraft facility.

Unsecured Loans

Loan from Friends

Unsecured loans taken from friends.

Unsecured Loans

Loan from Relatives

Unsecured loans taken from relatives.

Suspense Account

Suspense

Temporary account for uncertain or incomplete transactions.

Stock-in-Hand

Finished Goods

Value of goods that are ready for sale.

Stock-in-Hand

Raw Materials

Value of raw materials held in inventory.

Stock-in-Hand

Work in Progress

Value of unfinished goods in the production process.